3 Reasons RTX is Risky and 1 Stock to Buy Instead

Even during a down period for the markets, RTX has gone against the grain, climbing to $132.82. Its shares have yielded a 9.6% return over the last six months, beating the S&P 500 by 11%. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in RTX, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Despite the momentum, we don't have much confidence in RTX. Here are three reasons why RTX doesn't excite us and a stock we'd rather own.

Why Is RTX Not Exciting?

Originally focused on refrigeration technology, Raytheon (NSYE:RTX) provides a a variety of products and services to the aerospace and defense industries.

1. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect RTX’s revenue to rise by 4.6%, a deceleration versus its 9.7% annualized growth for the past two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

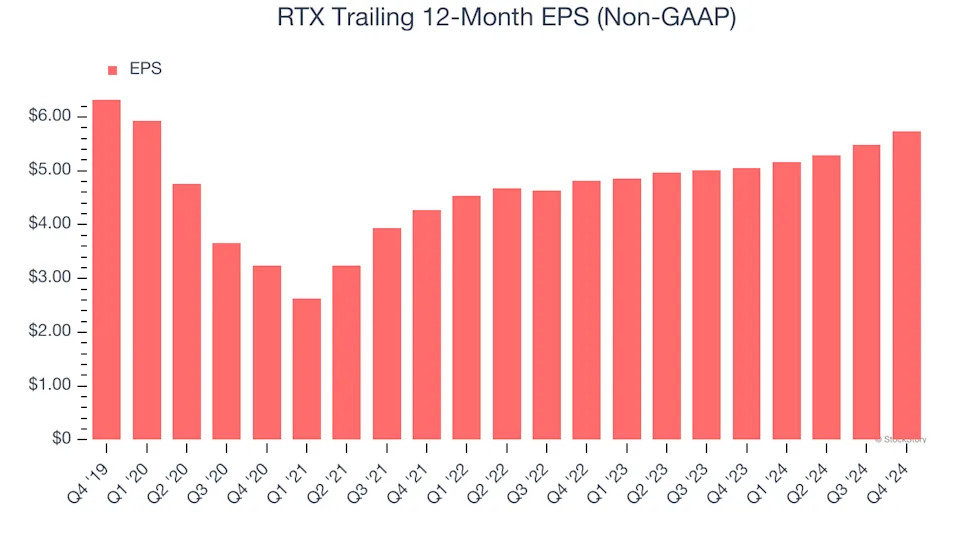

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for RTX, its EPS declined by 1.9% annually over the last five years while its revenue grew by 9.2%. This tells us the company became less profitable on a per-share basis as it expanded.

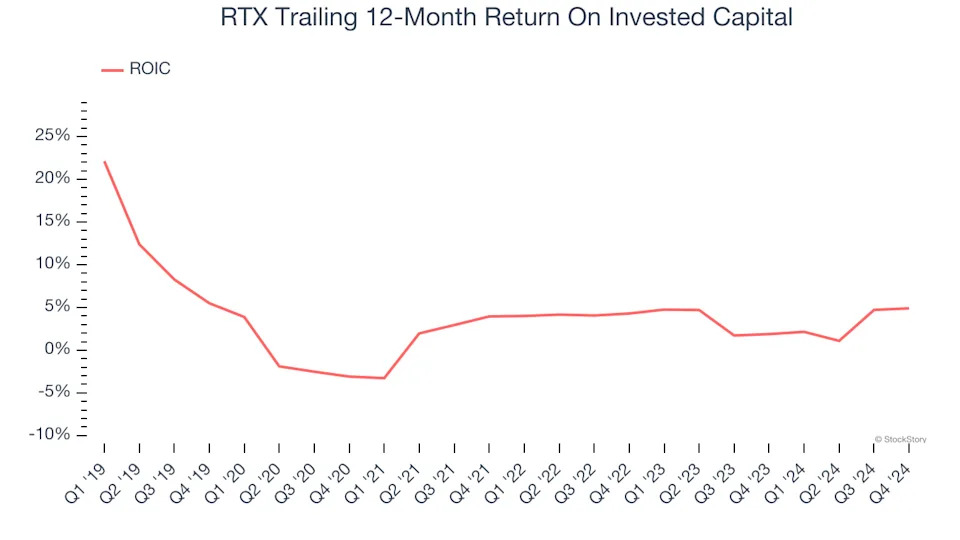

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

RTX historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.4%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

Final Judgment

RTX isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 21.8× forward price-to-earnings (or $132.82 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle .

Stocks We Would Buy Instead of RTX

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free .