All these market indicators point to stocks struggling during Trump’s presidency

On his first day in office, President-elect Donald Trump is likely to confront a U.S. stock market that is more overvalued than on any other Inauguration Day in U.S. history.

Since Trump famously views the stock market as a barometer of his success, he has his work cut out for him if the market over the next four years is to perform even as well as its historical average.

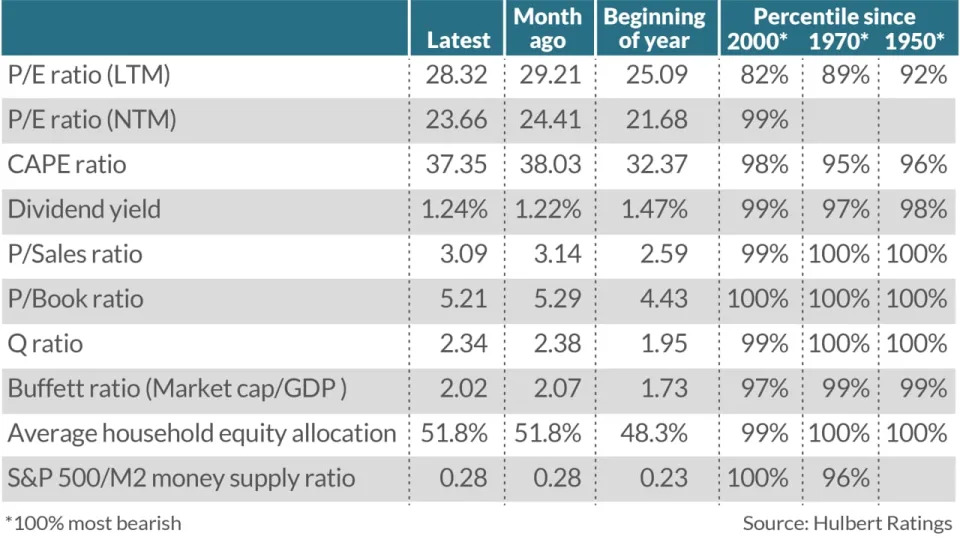

Consider the implicit forecasts of the valuation indicators listed in the table below. Though they qualified for that table because of their ability to forecast the U.S. market’s 10-year expected return, they also have respectable records forecasting four-year returns. On average, they implicitly are forecasting that the stock market will merely keep up with inflation between now and Inauguration Day in January 2029.

Of the indicators in this table, the one with the most statistically significant record when forecasting four-year returns is the equity allocation of the average U.S. household.

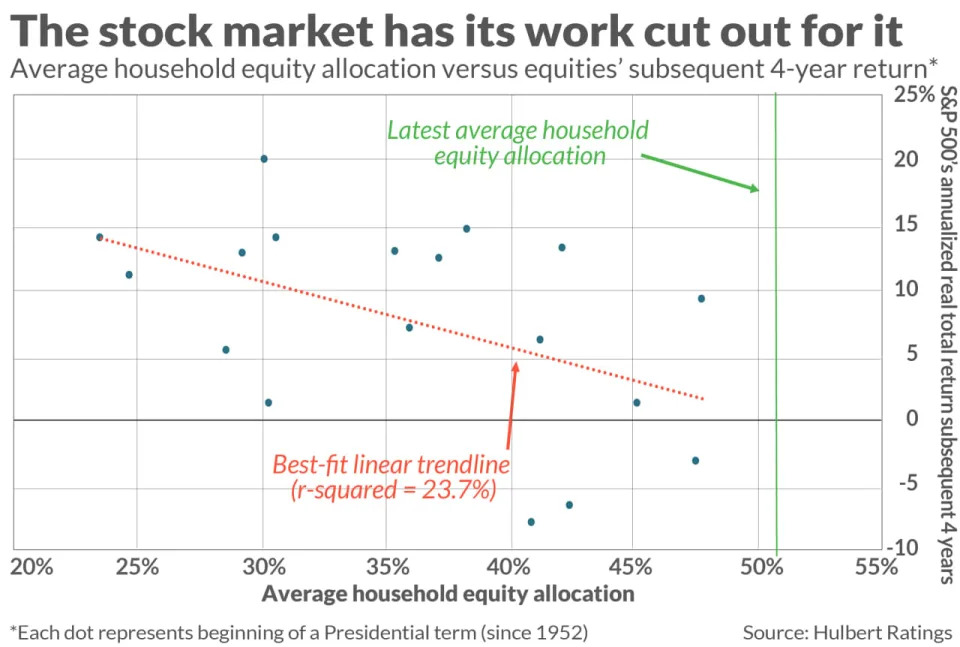

The chart below pinpoints where this indicator stood on each Inauguration Day beginning in 1952, along with the stock market’s inflation-adjusted total return over the subsequent four years. Notice the steep downwardly sloping line that best fits the data, indicating that higher average household equity allocations are associated with lower subsequent-four-year returns.

You will also notice in the chart the vertical green line indicating the current level of the average household equity allocation — 51.8% versus 48.3% at the beginning of 2024. An extrapolation of the chart’s trendline points to a real total return of minus 1.5% annualized over the next four years.

History doesn’t repeat, but it often rhymes. As the chart illustrates, there is still a lot of noise in the data despite the statistically significant downtrend. The previous record high for household equity allocation on Inauguration Day was in 2020, and yet since then the S&P 500 after inflation has produced a 9.3% annualized total return, which is above its 7.2% real-return average since 1952.

Still, it would be fair to say that the valuation winds won’t blow favorably for stocks over the next four years. The table above shows where each of the indicators I regularly monitor now stands relative to its historical distribution, over three different historical periods — since 2000, 1970, and 1950. With 100% being the most bearish, almost all of the readings are above 90%, with many at 100%.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at

More: The coming global interest-rate collapse will force four Fed rate cuts in 2025

Also read: Stock market will find it hard to rally unless the dollar and bonds calm down