Q4 Earnings Highs And Lows: Amkor (NASDAQ:AMKR) Vs The Rest Of The Semiconductor Manufacturing Stocks

The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Amkor (NASDAQ:AMKR) and the rest of the semiconductor manufacturing stocks fared in Q4.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 24.7% since the latest earnings results.

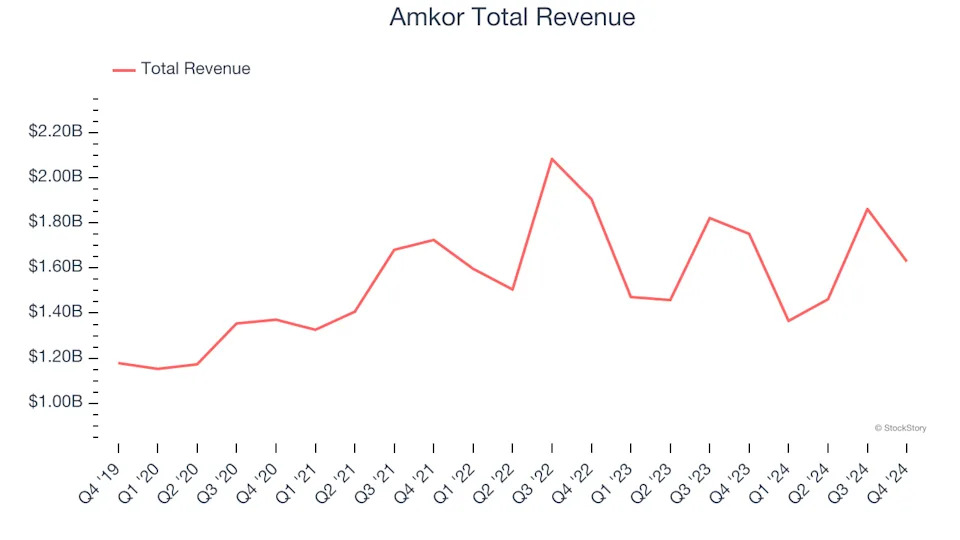

Amkor (NASDAQ:AMKR)

Operating through a largely Asian facility footprint, Amkor Technologies (NASDAQ:AMKR) provides outsourced packaging and testing for semiconductors.

Amkor reported revenues of $1.63 billion, down 7% year on year. This print fell short of analysts’ expectations by 2.1%, but it was still a satisfactory quarter for the company with a solid beat of analysts’ EPS estimates but an increase in its inventory levels.

“In 2024, weakness in the automotive and industrial and communications end markets contributed to a full year decline. In contrast, we achieved record revenue in our computing end market with growth in ARM-based PCs and AI devices,” said Giel Rutten, Amkor’s president and chief executive officer.

Amkor delivered the weakest performance against analyst estimates of the whole group. The stock is down 34.9% since reporting and currently trades at $15.85.

Is now the time to buy Amkor? Access our full analysis of the earnings results here, it’s free .

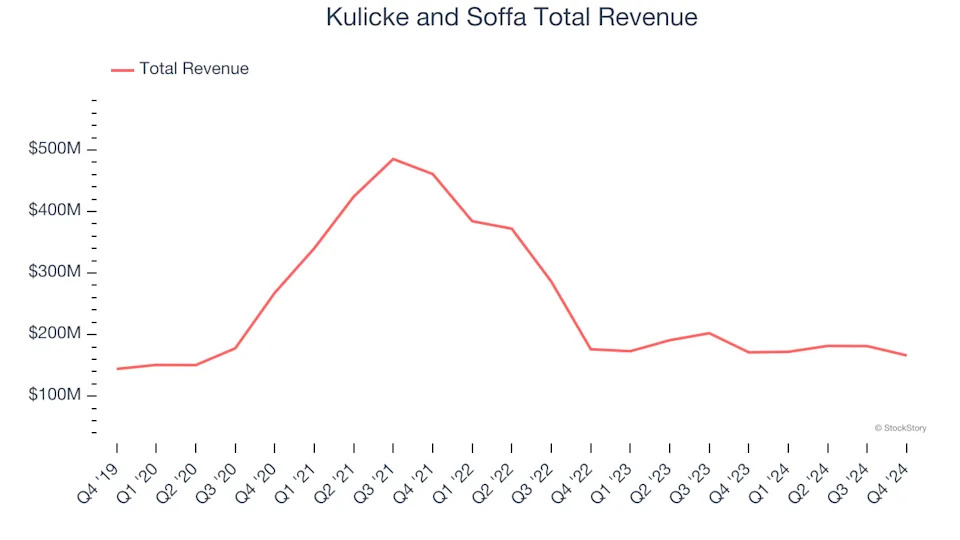

Best Q4: Kulicke and Soffa (NASDAQ:KLIC)

Headquartered in Singapore, Kulicke & Soffa (NASDAQ: KLIC) is a provider of production equipment and tools used to assemble semiconductor devices

Kulicke and Soffa reported revenues of $166.1 million, down 3% year on year, outperforming analysts’ expectations by 0.7%. The business had a very strong quarter with a significant improvement in its inventory levels and an impressive beat of analysts’ EPS estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 30.9% since reporting. It currently trades at $29.97.

Is now the time to buy Kulicke and Soffa? Access our full analysis of the earnings results here, it’s free .

Weakest Q4: FormFactor (NASDAQ:FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ:FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $189.5 million, up 12.7% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a significant miss of analysts’ adjusted operating income and EPS estimates.

As expected, the stock is down 38.2% since the results and currently trades at $25.43.

Read our full analysis of FormFactor’s results here.

IPG Photonics (NASDAQ:IPGP)

Both a designer and manufacturer of its products, IPG Photonics (NASDAQ:IPGP) is a provider of high-performance fiber lasers used for cutting, welding, and processing raw materials.

IPG Photonics reported revenues of $234.3 million, down 21.6% year on year. This print topped analysts’ expectations by 3.4%. It was a strong quarter as it also logged a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

IPG Photonics had the slowest revenue growth among its peers. The stock is down 18.3% since reporting and currently trades at $55.

Read our full, actionable report on IPG Photonics here, it’s free.

Marvell Technology (NASDAQ:MRVL)

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell Technology reported revenues of $1.82 billion, up 27.4% year on year. This number beat analysts’ expectations by 1.2%. More broadly, it was a slower quarter as it logged revenue guidance for next quarter slightly missing analysts’ expectations and an increase in its inventory levels.

The stock is down 38.4% since reporting and currently trades at $55.59.

Read our full, actionable report on Marvell Technology here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here .