Dollar Tree (NASDAQ:DLTR) Misses Q4 Sales Targets, But Stock Soars 7.2%

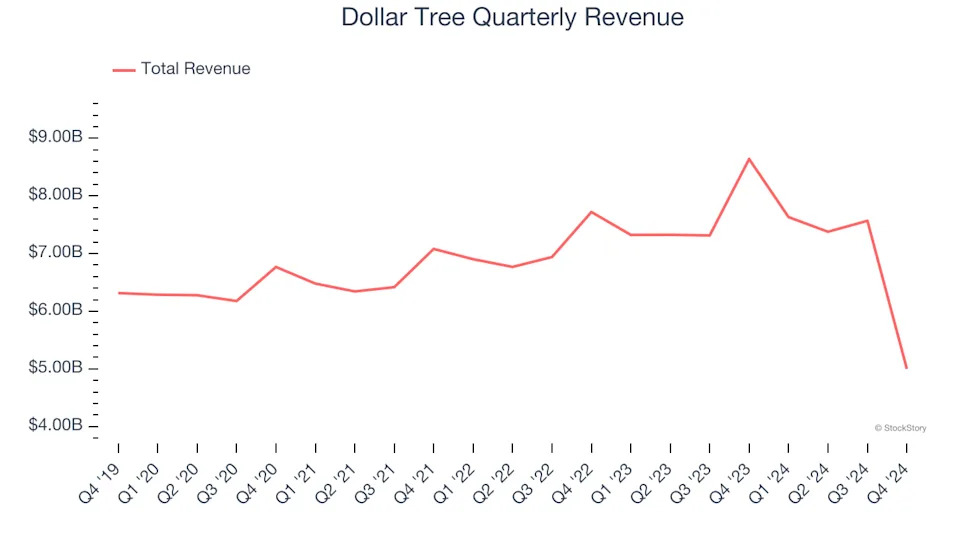

Discount treasure-hunt retailer Dollar Tree (NASDAQ:DLTR) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 42.1% year on year to $5 billion. Next quarter’s revenue guidance of $4.55 billion underwhelmed, coming in 42.1% below analysts’ estimates. Its non-GAAP profit of $2.29 per share was 4.3% above analysts’ consensus estimates.

Is now the time to buy Dollar Tree? Find out in our full research report .

Dollar Tree (DLTR) Q4 CY2024 Highlights:

“In the fourth quarter, our team was focused on successfully closing out the year, bringing the strategic review to a favorable conclusion, and setting Dollar Tree on a path to realize its full potential to create long-term value for our associates, customers, and shareholders,” said Mike Creedon, Chief Executive Officer.

Company Overview

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ:DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

Discount Grocery Store

Traditional grocery stores are go-tos for many families, but discount grocers serve those who may not have a traditional grocery store nearby or who may have different spending thresholds. Certain rural or lower-income areas simply don’t have a grocery store. Additionally, some lower-income families would prefer to buy in smaller quantities than available at most stores (think one or two paper towel rolls at a time). While online competition threatens all of retail, grocery is one of the least penetrated because of the nature of buying food. Furthermore, those buying small quantities for immediate need are even less likely to leverage e-commerce for these purposes.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $27.58 billion in revenue over the past 12 months, Dollar Tree is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. For Dollar Tree to boost its sales, it likely needs to adjust its prices or lean into foreign markets.

As you can see below, Dollar Tree grew its sales at a sluggish 3.2% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as its store footprint remained unchanged.

This quarter, Dollar Tree missed Wall Street’s estimates and reported a rather uninspiring 42.1% year-on-year revenue decline, generating $5 billion of revenue. Company management is currently guiding for a 40.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.9% over the next 12 months, an acceleration versus the last five years. This projection is eye-popping for a company of its scale and suggests its newer products will fuel better top-line performance.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Store Performance

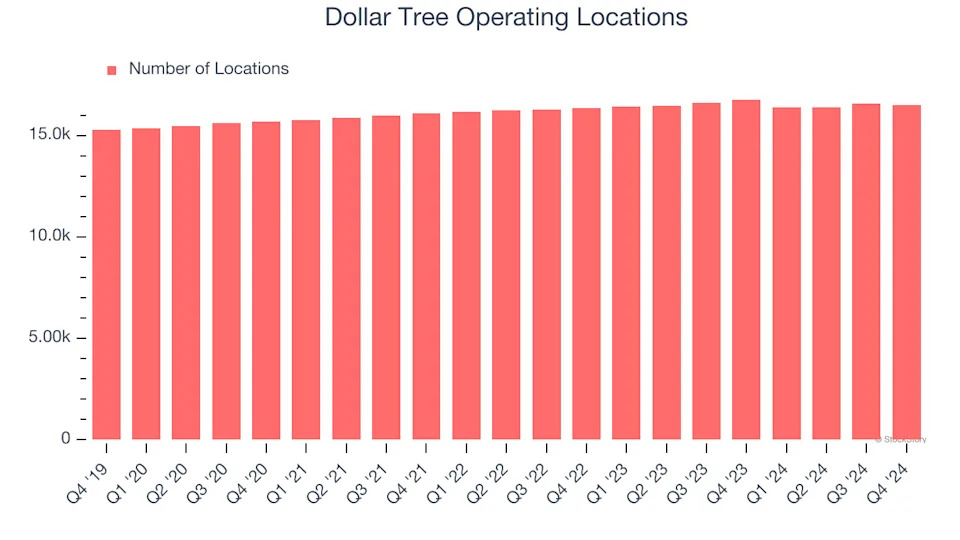

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Dollar Tree listed 16,503 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

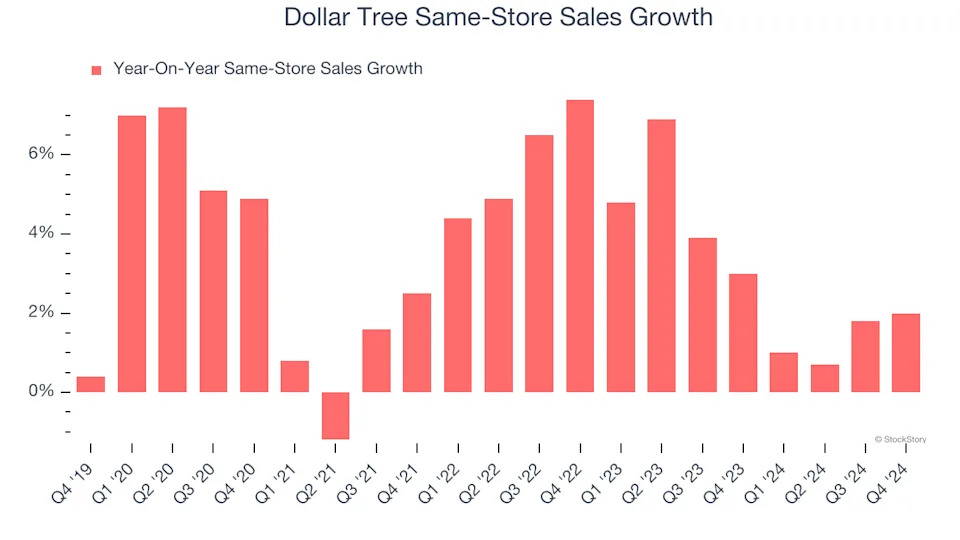

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Dollar Tree’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Dollar Tree’s same-store sales rose 2% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Dollar Tree’s Q4 Results

The result this quarter don't matter as much as the company's announcement to sell its Family Dollar unit, which it acquired in 2015. The stock traded up 3.8% to $69.73 immediately after reporting.

So do we think Dollar Tree is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .