3 Reasons LESL is Risky and 1 Stock to Buy Instead

Leslie's has gotten torched over the last six months - since September 2024, its stock price has dropped 64.2% to $1.05 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Leslie's, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Despite the more favorable entry price, we're swiping left on Leslie's for now. Here are three reasons why LESL doesn't excite us and a stock we'd rather own.

Why Is Leslie's Not Exciting?

Named after founder Philip Leslie, who established the company in 1963, Leslie’s (NASDAQ:LESL) is a retailer that sells pool and spa supplies, equipment, and maintenance services.

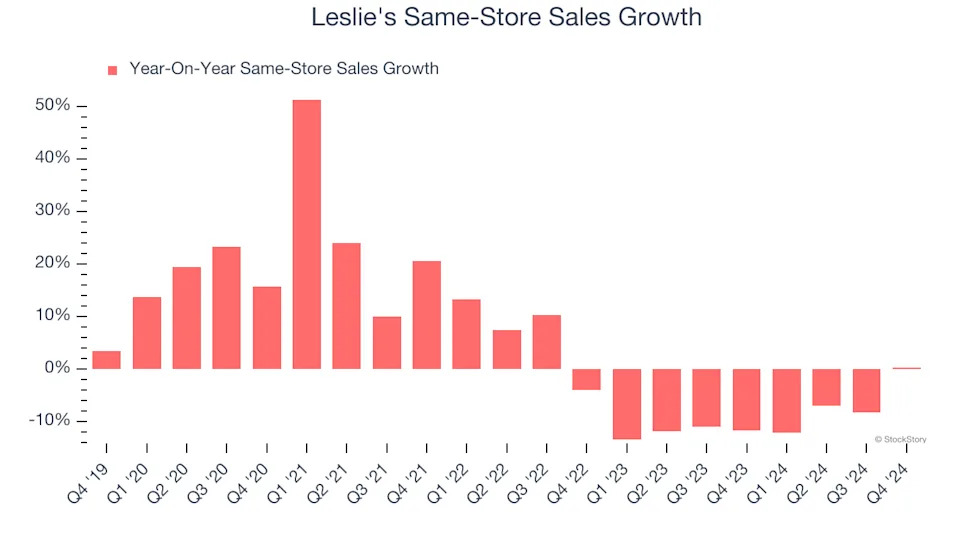

1. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Leslie’s demand has been shrinking over the last two years as its same-store sales have averaged 9.4% annual declines.

2. Fewer Distribution Channels Limit its Ceiling

With $1.33 billion in revenue over the past 12 months, Leslie's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

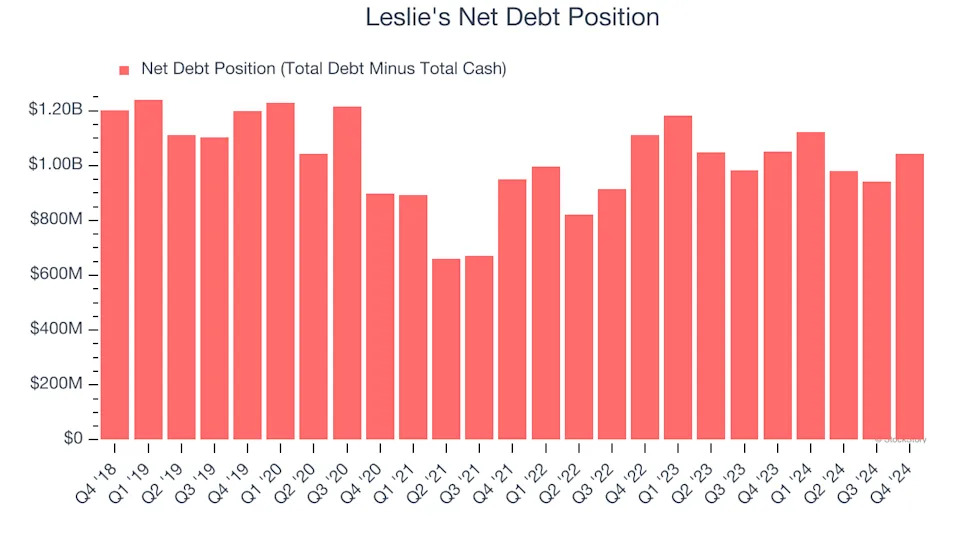

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Leslie’s $1.05 billion of debt exceeds the $11.62 million of cash on its balance sheet. Furthermore, its 10× net-debt-to-EBITDA ratio (based on its EBITDA of $103.8 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Leslie's could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Leslie's can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Leslie's isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 16.3× forward price-to-earnings (or $1.05 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of Charlie Munger’s all-time favorite businesses .

Stocks We Like More Than Leslie's

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month . This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free .