Sleep Number (NASDAQ:SNBR) Misses Q4 Revenue Estimates, Stock Drops

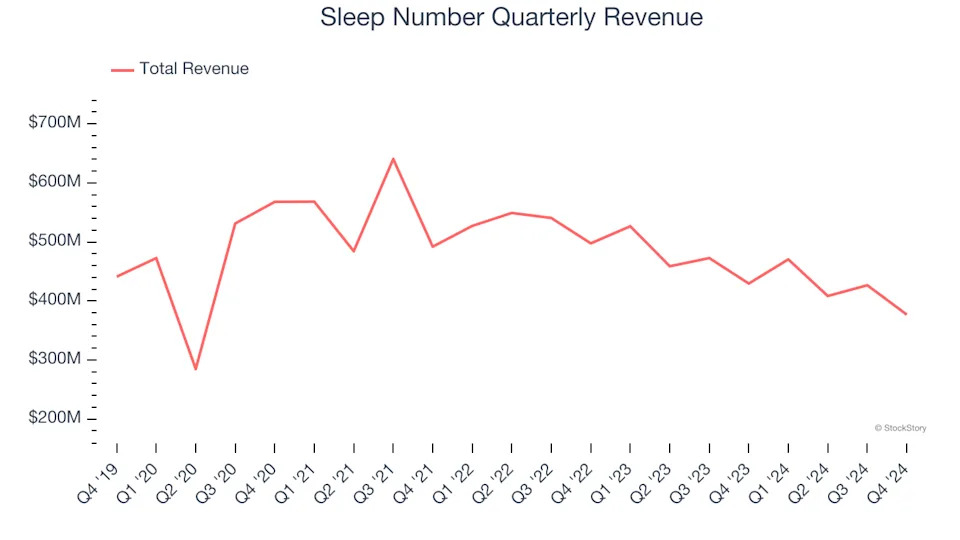

Bedding manufacturer and retailer Sleep Number (NASDAQ:SNBR) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 12.3% year on year to $376.8 million. Its GAAP loss of $0.21 per share was 10.6% above analysts’ consensus estimates.

Is now the time to buy Sleep Number? Find out in our full research report .

Sleep Number (SNBR) Q4 CY2024 Highlights:

Company Overview

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ:SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.68 billion in revenue over the past 12 months, Sleep Number is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sleep Number struggled to increase demand as its $1.68 billion of sales for the trailing 12 months was close to its revenue five years ago (we compare to 2019 to normalize for COVID-19 impacts). This was mainly because it didn’t open many new stores.

This quarter, Sleep Number missed Wall Street’s estimates and reported a rather uninspiring 12.3% year-on-year revenue decline, generating $376.8 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months. While this projection implies its newer products will spur better top-line performance, it is still below the sector average.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Store Performance

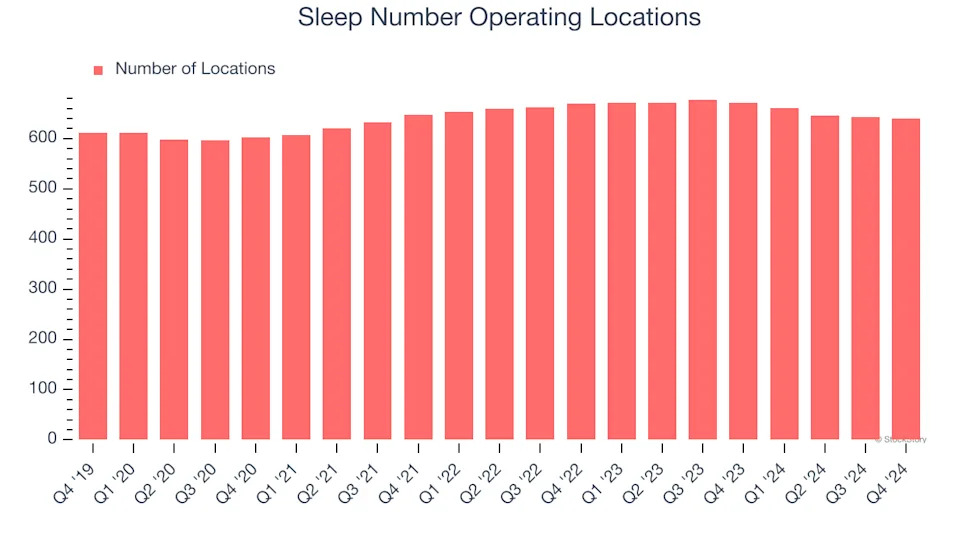

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Sleep Number operated 640 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Sleep Number’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Sleep Number starts opening new stores to artificially boost revenue growth.

In the latest quarter, Sleep Number’s same-store sales fell by 12% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Sleep Number’s Q4 Results

It was encouraging to see Sleep Number beat analysts’ EPS expectations this quarter. We were also happy its gross margin narrowly outperformed. On the other hand, its EBITDA missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 8.7% to $11.80 immediately following the results.

Sleep Number underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free .